Business 401(k) Services / Plan Administration

What Is a 401(k) Fiduciary?

If you make decisions for your company’s 401(k), you are a fiduciary. Every retirement plan needs at least one trusted, reliable fiduciary, someone who works in the best interest of the plan and its participants. To better understand your role as a fiduciary, consider these common questions.

What Is the Definition of a Fiduciary?

If you make decisions on behalf of a retirement plan, you’re a fiduciary and are required by law to act in the best interest of the plan. This means following all requirements and regulations, offering a diverse selection of investments, managing plan assets responsibly, making sure fees and other costs are reasonable, and more. Fiduciaries who do not uphold their fiduciary duties are personally liable and could face fines.

What Is Fiduciary Responsibility?

As a fiduciary, you’re expected to act prudently and to consider how your decisions will affect plan participants. It also means you need to have administrative systems in place that document your decisions and communicate important details to participants.

If you don’t meet your fiduciary responsibilities, you may be liable for harm caused by your decisions. Fiduciary mismanagement could cost you and your company tens of thousands of dollars in legal fees and fines.

What Are the Different Types of Fiduciaries?

There are three types of retirement plan fiduciaries.

- A 3(38) investment manager is a fiduciary who is responsible for selecting, monitoring, and updating all investment options available to the plan with discretion. They take responsibility for plan investment decisions. Your responsibility is to select and oversee your fiduciary.

- A 3(21) investment adviser is a co-fiduciary, which means they make investment recommendations, but the ultimate decision is up to you and you’re still responsible and liable for the decisions made.

- A 3(16) administrative fiduciary is responsible for fulfilling specific administrative duties on behalf of the plan. For example, a 3(16) administrative fiduciary signs and files Form 5500 with the Department of Labor and approves loans.

What Is a 3(16) Administrator?

A 3(16) fiduciary is responsible for the administrative side of the plan. This is different from a 3(38) investment manager, who is responsible for making plan-level investment decisions. A 3(16) administrator might:

- Determine employee eligibility

- Provide disclosures to employees and other participants

- Provide statements to employees and other participants

- Fix errors in the plan leading to compliance test, nondiscrimination test, and ADP/ACP test failure

- Sign and file annual 5500 forms

- Approve and process loans and distributions

Note that not all 3(16) administrator partners will handle 100% of these duties. And there may be other services a provider offers that aren’t technically fiduciary services. Employers may retain some of the duties of a plan administrator, or may choose to delegate some or all of them to an employee, like an HR manager.

What Is a 401(k) Plan Fiduciary?

A 401(k) plan fiduciary is anyone who makes decisions on behalf of the plan. For example, someone who signs plan-level documents, makes plan-level investment decisions, or plan design decisions is typically considered a fiduciary.

What Is Fiduciary Liability?

Being a fiduciary means you’re liable if something goes wrong with your plan. When considering your liability, understand:

- Ignorance is no defense in a court of law.

- A fiduciary is personally liable to make good on plan losses due to an ERISA provision breach.

- The Department of Labor may assess a civil penalty equal to 20% of the recovery amount.

- Individuals may be fined up to $100,000 and jailed up to 10 years for ERISA violations.

- Companies may face up to $500,000 in fines for ERISA violations.

Can I Outsource Some Fiduciary Duties?

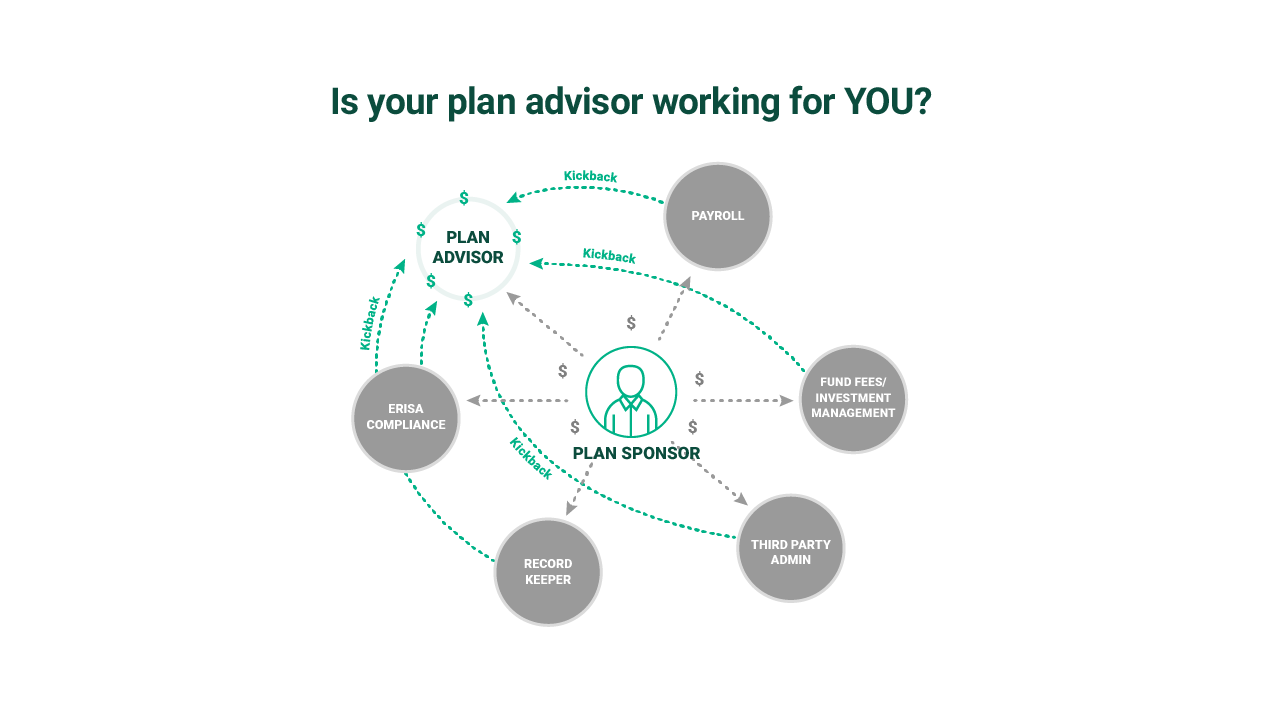

Yes, you can outsource many fiduciary duties including investment management and administrative tasks. Outsourcing fiduciary duties can reduce both your liability and administrative burden. Some retirement plan providers, third-party administrators, or recordkeepers offer fiduciary services. If you consider outsourcing with a fiduciary, find out exactly what services they offer and what responsibilities remain with you. Some claim to be full fiduciaries but leave critical duties up to you. Watch out for fiduciaries who:

- Have incentive structures that include revenue sharing or kickbacks.

- Don’t help and maintain a fiduciary audit file.

- Don’t offer fiduciary education for your plan committee.

As a 3(38) investment manager, Fisher maintains the highest fiduciary standards and will partner with you to make sure you, your company, and your employees are protected.

Partner with Fisher

Fisher Investments has been a fiduciary partner to small and medium-sized businesses for a decade. Contact us to learn more about how we can partner with you to protect your company and employees.

See our Business 401(k) Insights

Resources and articles to help your business with retirement plan support, optimization and administration.

Business 401(k) Resources by Topic

-

401(k) Plan Optimization Your Interests First1/1/2023 12:00:00 AM

-

Plan Administration How to Find the Best 401(k) Provider1/1/2023 12:00:00 AM

-

Plan Administration 401(k) Employee Services1/1/2023 12:00:00 AM

-

401(k) Plan Optimization Investment Analysis1/1/2023 12:00:00 AM

Contact Us

One of our 401(k) business specialists would love to talk to you about your company’s retirement plan needs.

Call Us

Get Me Started