Business 401(k) Services / Plan Administration

401(k) Administration at Your Small Business

Ideally, you have an adviser or other plan partner to help you or your 401(k) plan manager keep track of deadlines. But for those who don’t, we’ve put together a list of your administrative duties as a 401(k) plan manager. From filing paperwork to monitoring and coordinating with your service providers, read each section below to learn more about running your business’s 401(k) plan.

Select & Monitor Your Service Providers

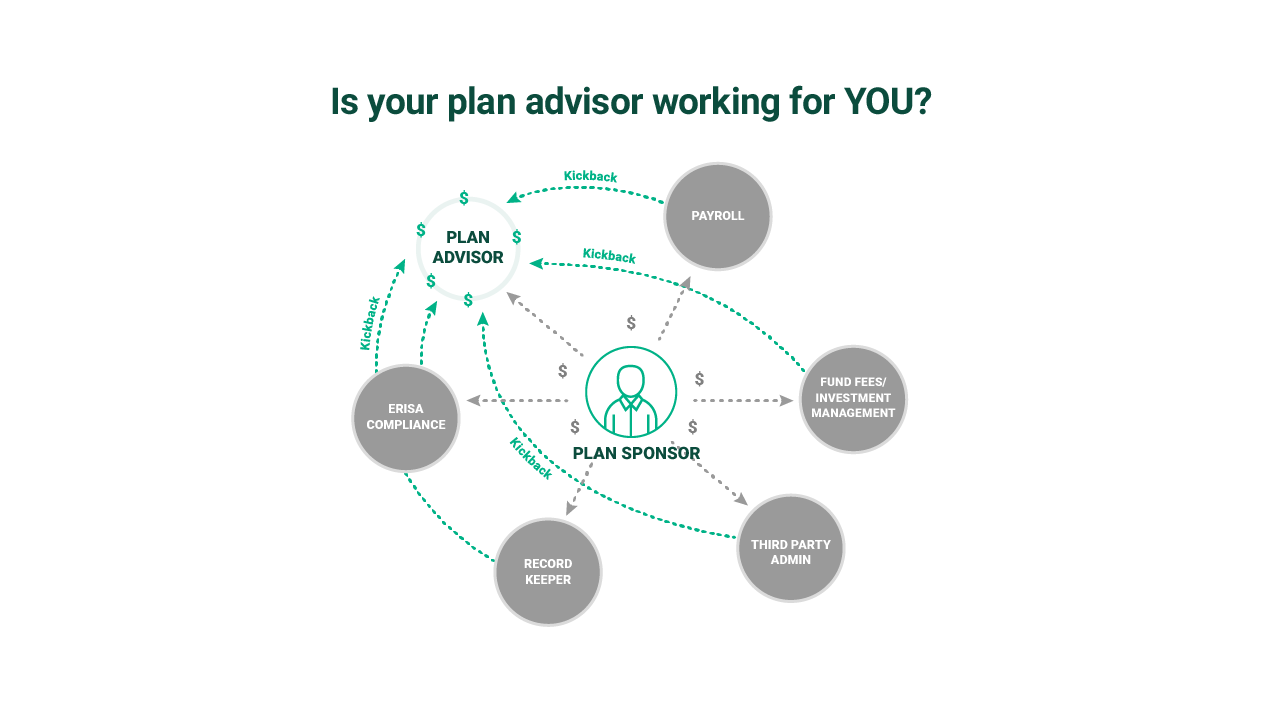

If you run your company 401(k) plan, you are one of the plan’s fiduciaries, which means you’re a key decision-maker and help operate the plan. Part of operating the plan is choosing and monitoring the service providers who serve the plan, which usually includes your adviser, the recordkeeper, and the third party administrator. Here are a couple things to keep in mind:

- When it comes to selecting and monitoring those providers, having a documented process is perhaps the most important step. Documenting why you chose certain service providers is a protective measure that shows you’re acting “prudently”—you have specific reasons for choosing who you did. Along with this, it’s also important to know what your service agreements with those providers do and don’t cover, that way you can monitor whether your service providers are performing all of their stated duties for your plan.

- How do you know you’re paying a fair price for your plan services? Another part of the selection and monitoring process is making sure you or your employees are receiving good support for the fees you’re paying. Unreasonably-high plan fees are a negative for two reasons:

- Usually, employees pay most of the fees in a 401(k) plan, and high fees can eat into the investment returns they should be receiving. They’ll be relying on that money during retirement, and most family retirement balances are already under-funded—they’ll need as much as they can.1

- Excessively-high fees can open up an employer to lawsuits. If the employer chooses to forego a lower-cost provider option in favor of a more expensive one without a good, documented reason, the employer can be held liable for the investment returns lost due to those excessive fees.

Follow the Plan Documents

The 401(k) plan manager should create a plan document and follow it—these are documents that act as a roadmap to running the plan. The features outlined in your plan document should align with your business needs; if your 401(k) plan is not serving you and your employees the way you wanted it, request a plan review from your adviser.

Ideally, the adviser would proactively review your plan document with you (and other important stakeholders).

Communicate and Coordinate with Your Service Providers

Every retirement plan has key dates to follow for filing paperwork. Most of this paperwork has to do with making sure your documents and employee information are in order; bad employee census data or employer contribution information can “poison the well” and affect the rest of your plan data. For example, inaccurate employee census information will mean that your annual compliance testing results are inaccurate as well, which means you might face additional obligations or restrictions to your plan until it passes.

Communicating and coordinating with service providers can be a time-consuming aspect of running the plan. An adviser who will coordinate the following on your behalf can save you a lot of administrative work:

- Updating employee census data

- Monitoring employee loans and distributions

- Annual compliance testing assistance

- Filing your plan’s Form 5500

- Helping create your plan’s Investment Policy Statement

- Preparing some annual employee disclosures (for those who participate in the plan)

- Calculating employer contribution allocations if needed

- Making any necessary updates to your plan document to keep it current

401(k) Administration Best Practices

Some advisers will do a lot of your administrative work for you—including sending required disclosures to your employees on your behalf, or providing educational resources to your employees. But some steps should still be completed by you or the person at your company responsible for managing the 401(k) plan. For example, you may have an adviser who helps put together your Form 5500, but the plan manager would still file that document with the government. Below are a few general 401(k) best practices to consider:

- Distribute employee disclosures in a timely manner—or hire a 3(16) Administrator to help you

- Disperse employee distributions in a timely manger

- File all required forms with the IRS annually

- Educate your employee base on the importance of participating in the plan—or consider an adviser who specializes in retirement education

- Retain copies of all plan documents

- Cover your plan with a Fidelity Bond

- Meet annually with your 401(k) plan committee (or plan stakeholders) to review the plan, and confirm that it’s working the way it’s intended

- Take notes during your 401(k) committee meetings, and keep those as documentation of your management process

Even with this information, it can still be difficult to make sure all your 401(k) ducks are in a row. If you have more questions about administering a 401(k), take a look at our article about how to avoid common 401(k) administration issues, or contact us to speak with a 401(k) specialist.

1The Continuing Retirement Savings Crisis. National Institute on Retirement Security. March 2015. https://www.nirsonline.org/reports/the-continuing-retirement-savings-crisis/

See our Business 401(k) Insights

Resources and articles to help your business with retirement plan support, optimization and administration.

SHARE THIS MEDIA

Business 401(k) Resources by Topic

-

401(k) Plan Optimization Your Interests First1/1/2023 12:00:00 AM

-

Plan Administration How to Find the Best 401(k) Provider1/1/2023 12:00:00 AM

-

Plan Administration 401(k) Employee Services1/1/2023 12:00:00 AM

-

401(k) Plan Optimization Investment Analysis1/1/2023 12:00:00 AM

Contact Us

One of our 401(k) business specialists would love to talk to you about your company’s retirement plan needs.

Call Us

Get Me Started