Business 401(k) Services / Start a 401(k)

How To Start A 401(k) Plan For Your Business

1. Decide On A Plan That’s Right For Your Business

The word “401(k)” is used to represent a variety of retirement plans—you’re not stuck with just one kind, you have many choices. Each plan type provides different benefits for yourself, your employees, and your business. With a traditional 401(k), participants in the plan contribute a percentage or set amount of income before taxes. As the employer, you can contribute money to your employees’ accounts in a variety of ways. There are three main types of retirement plans:

- Traditional 401(k): Offers a lot of flexibility for employee contributions, vesting schedules (which allow the owner to determine when the employees have access to employer contributions to their retirement accounts), and employer matching contributions.

- 401(k) with Safe Harbor: Allows the plan to bypass some government tests in exchange for a set employer contribution percentage.

- 401(k) with Profit Sharing: Allows the employer to award 401(k) contributions to employees based on how profitable the company was in a given year, as well as bonus compensation based on employee performance or the importance of their role in the company.

- Start a 401(k)

Additionally, there are many features you can add to a 401(k) to make it a better benefit for your business and employees. Some features that you may want to add to your plan include:

- Automatic employee enrollment: Enrolls your employees into your 401(k) automatically with a contribution amount that each employee can adjust.

- Matching contributions: Gives the business owner the option to match 401(k) contributions made by the employee.

- 401(k) loans: Allows employees to borrow money from their 401(k) account.

- A Roth option: Allows employees to contribute money to their 401(k) post-tax, as opposed to the pretax contributions that are typically made.

- Auto-escalation: Automatically increases employee contributions to the plan.

- Employee eligibility requirements: The owner can establish eligibility requirements, such as a minimum number of months of employment for employee participation in the company 401(k).

2. Choose A 401(k) Plan Provider

After you have an idea of what type of 401(k) plan you’d like to establish, it’s time to pick a provider. Many financial institutions offer small business 401(k) plans to some degree, but there are a few things to look out for:

- Fees and other expenses. There are many expenses associated with a 401(k), which are usually paid by participants in the plan. See more on this below.

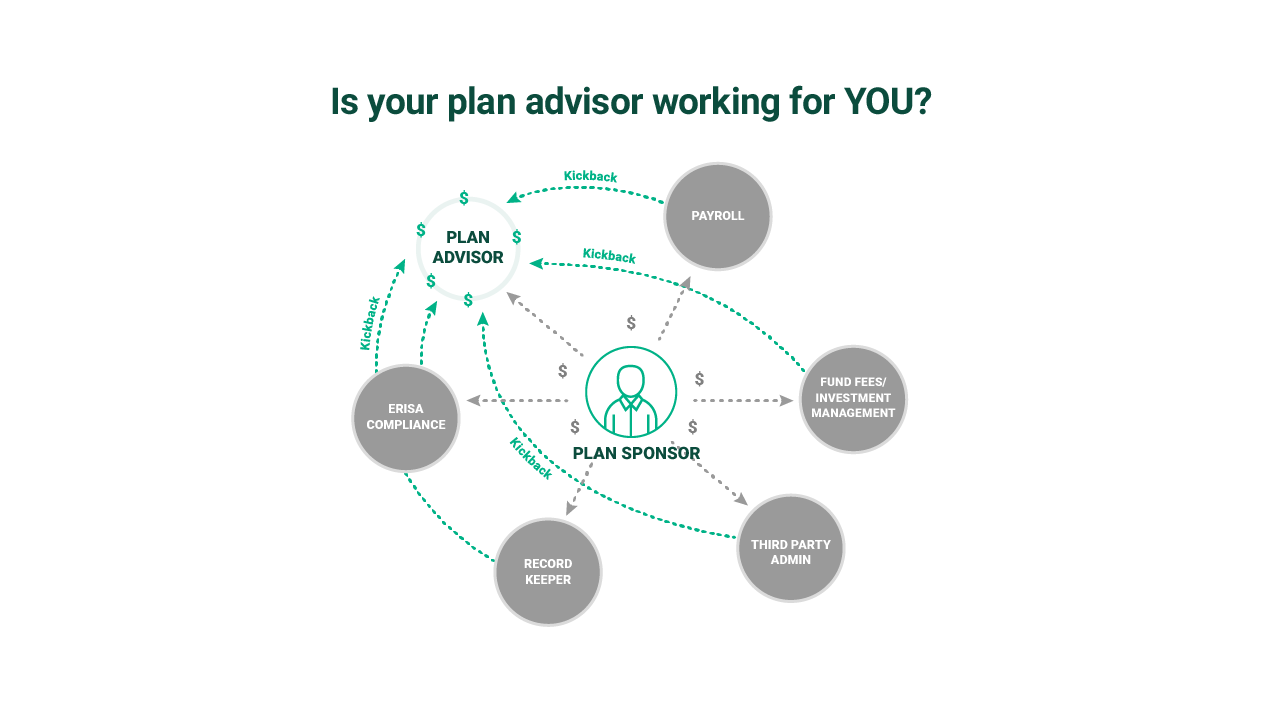

- Fiduciary protection. The plan fiduciary is the person in charge of making decisions on behalf of the plan—usually the business owner or another executive. And while plan decisions ultimately fall on your shoulders, certain types of plan providers will allow you to delegate some of your legal responsibilities to them. For example, providers designated as 3(38) Investment Managers will take responsibility for selecting and monitoring your fund line-up.

- Investment bias. Some brokers may recommend their own funds or other products because they receive additional compensation for selling them. A recent rule change by the DOL that requires brokers and other financial advisers to act in your best interest will mitigate the risk of conflicts of interest regarding investments, but hiring an independent investment adviser may help give you an objective look at everything the market has to offer. The rule takes effect April 2017.

- Employee education and ongoing support. Planning for retirement can be difficult and overwhelming if you’re starting from square one; choosing a provider who can help your employees set up retirement investments that match their own unique situation and individual needs can boost employee confidence that they’re on the right track. And because not all employees will feel comfortable after a single session—and you may have new hires that need help—continuing education and ongoing support become that much more important.

3. Carefully Examine The Fees

There will be operating costs for any 401(k) plan, which will vary based on who you choose to be your plan administrator and plan service provider. There are several types of fees to look out for, so it’s important to do your due diligence in determining the total cost to you and your employees for operating the plan. In particular, look at the administrative fees, financial adviser fees, and fund fees to get an idea of what you’ll be paying for the 401(k) and your investments.

You are ultimately on the hook for making sure that the fees you and your employees are being charged are “reasonable” for the services provided, so examine the fees carefully and make sure you aren’t being charged for something that isn’t providing a benefit.

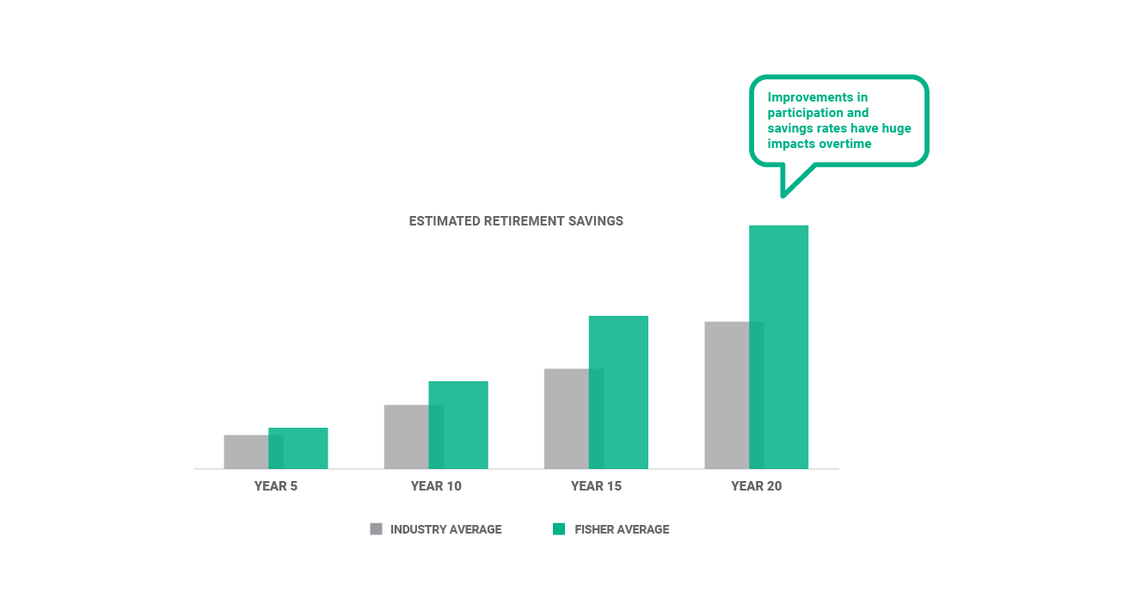

Over several decades, fees that may not seem high can take huge chunks out of your retirement income—so do your due diligence!

4. Make Sure Your Plan Benefits All Participants

A 401(k) is meant to benefit all participants. In order to ensure this, all plans need to pass annual tests designed to verify that the plan does not unfairly benefit only the highest earning employees. These tests are referred to as non-discrimination tests. If you decide to start a 401(k) plan with a safe harbor feature, good news: Many safe harbor plans automatically pass non-discrimination tests—they offer a guaranteed benefit for all employees. For most other types of plans though, non-discrimination tests will be performed to look at your plan and make sure that it’s fair to all employees.

5. Don’t Rush Into A Plan Just To Have One

Doing your proper due diligence—carefully examining the pros and cons of each type of plan, and meeting with several service providers—can help you feel confident that you’re picking the right plan for your business. Once you find a fee schedule and service offering that works for your business and employee needs, you’ll feel more comfortable knowing that you’ve got a plan that you and your employees can be proud of.

If you would like to learn more about some of the tax benefits of starting a 401(k) plan for your business, click here.

See our Business 401(k) Insights

Resources and articles to help your business with retirement plan support, optimization and administration.

Business 401(k) Resources by Topic

-

401(k) Plan Optimization Your Interests First1/1/2023 12:00:00 AM

-

Plan Administration How to Find the Best 401(k) Provider1/1/2023 12:00:00 AM

-

Plan Administration 401(k) Employee Services1/1/2023 12:00:00 AM

-

401(k) Plan Optimization Investment Analysis1/1/2023 12:00:00 AM

Contact Us

One of our 401(k) business specialists would love to talk to you about your company’s retirement plan needs.

Call Us

Get Me Started