Business 401(k) Services / Economics

Your 401(k) Plan Advisor: Are You Getting A Good Value?

Paying Less Now Isn't A Good Deal If It Costs You In Service And Performance Later.

As the sponsor of your company's 401(k) plan, you may be tempted to cut up-front costs by going with a plan advisor who charges lower fees.

But is that being penny wise and pound foolish? Depends on how much value your plan advisor brings to the table. It's important to understand what you should expect from a plan advisor for the fees they charge—and how that impacts the bottom line.

Here are four primary ways a plan advisor can create value for you and your plan participants, both now and in the long term:

Higher participation rates: Just because there's an option to take advantage of a 401(k) plan doesn't mean your employees will automatically participate. A good plan advisor will work one-on-one with employees to educate them about the long-term plan benefits, resulting in more employees becoming plan participants.

Higher deferral rates: A common mistake plan participants make is not deferring enough of their compensation into the plan at the start. A good plan advisor will show plan enrollees the outsize difference even 1% more in deferral can make to retirement savings over even just 20 years, and help participants see the wisdom in increasing their deferral rates at the start.

Investment performance: Many institutional plan advisors offer plans made up of mediocre investment options that are expensive and deliver lower growth. A good plan advisor will develop a high-quality investment line up and asset allocation that generates more wealth over the long term.

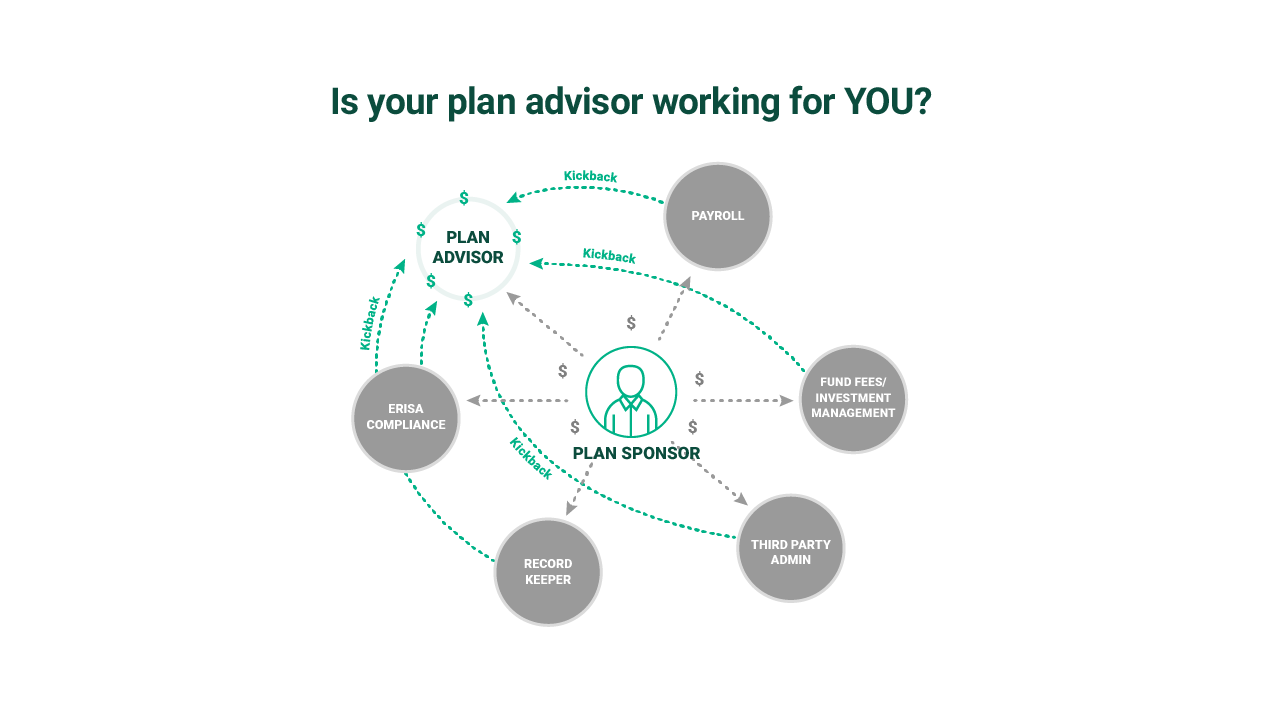

Transparent fees: A good plan advisor will offer a plan with a fee structure focused on generating wealth for you and your employees, not padding their own profits through high fees and revenue sharing agreements, which are kickbacks, incentives, or commissions from the funds or other partners in the 401(k) plan.

So What Can You Expect From A Low-Service 401(k) Provider?

To keep costs low, these providers often deliver only the lowest-common-denominator service required. Their plans are often one-size-fits-all approaches that leave many decisions to you or your employees to figure out on your own and aren't tailored to help generate as much wealth as possible. They also tend to offer only limited services, self-serve education, and fewer investment options specific to the needs or goals of your business and participants.

None of these drive value in the four ways explained above. And while this lower level of service might seem like it costs less, it can end up costing you and your employees much more over time.

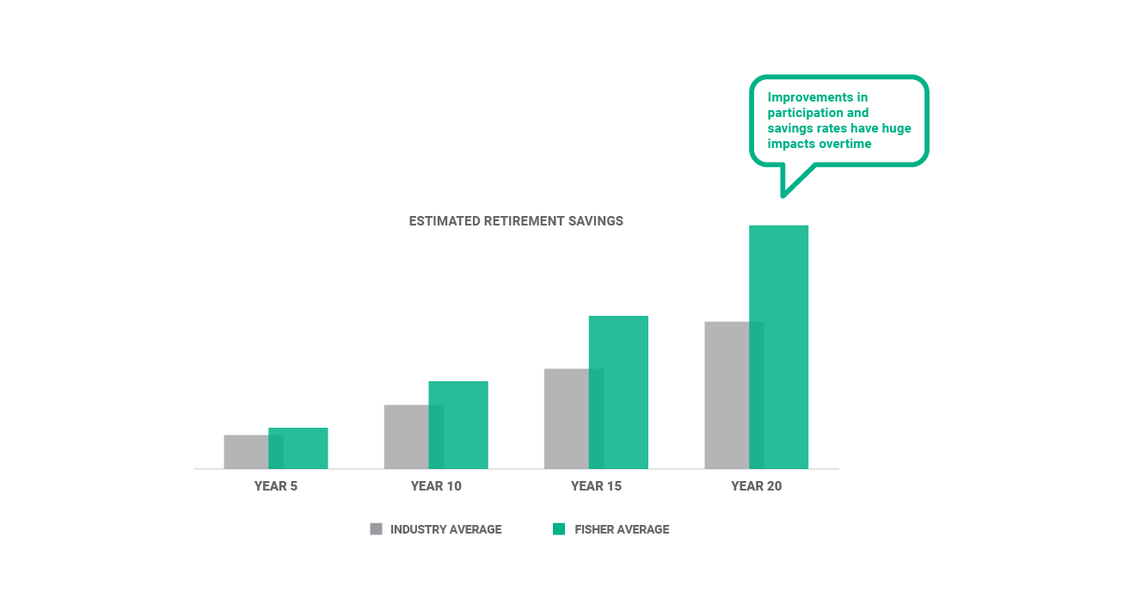

Consider this example: A plan sponsor chooses to go with a plan advisor that costs 0.25% less in fees. That low cost translates into poorer service and education, and as a result low participant and deferral rates. And because of the low-value, high-cost fund line up, participants end up paying 1% more in fund fees and earning 1% less in performance over time. The result? A staggering difference when compared over time with a high-value, high-service plan advisor.

Immediate savings may sound great, but in the end, you get what you pay for: low engagement, limited flexibility, and under-performance. Over time, these factors will negate any savings on the front end—and then some. You should always factor in long-term returns and costs alongside current savings of a low-cost plan.

Do you know if you're paying too much and getting too little from your plan advisor? Download our Complete Guide to 401(k) Costs to learn about fund fees, revenue sharing, and other costs that impact your plan and employees.

You can also contact Fisher for a free fee analysis and comparison of your 401(k). Contact us today.

See our Business 401(k) Insights

Resources and articles to help your business with retirement plan support, optimization and administration.

Business 401(k) Resources by Topic

-

401(k) Plan Optimization Your Interests First1/1/2023 12:00:00 AM

-

Plan Administration How to Find the Best 401(k) Provider1/1/2023 12:00:00 AM

-

Plan Administration 401(k) Employee Services1/1/2023 12:00:00 AM

-

401(k) Plan Optimization Investment Analysis1/1/2023 12:00:00 AM

Contact Us

One of our 401(k) business specialists would love to talk to you about your company’s retirement plan needs.

Call Us

Get Me Started